50% off all ESET Products on Black Friday!

If you’re in debt with credit cards, it’s time to make some hard and fast rules that will not only help you pay that debt down faster, it will turn your credit cards into powerful tools that will not only save you money – they will be a part of your income streams eventually.

Hopefully, by now, you’ve worked out exactly how much you owe on each card, and have chosen one to be your initial focal point. This is the card you will get paid down first – you will throw all your extra money at this debt until it’s gone.

This is the cardinal rule: if you owe money on a card, you are not allowed to use that card. Until it’s paid down, it’s in limbo – it exists, and you may even have a usable balance available – but you aren’t going to use it.

Once it’s paid down, I’ll show you how to use it wisely, as a tool to save you time, expedite your regular bill payments, and begin to work for your financial future, instead of against it.

This is nearly as (probably just as) important as Rule #1: Never, ever, ever take a cash advance on a credit card.

Ever.

Seriously, never do this. The interest rate on a cash advance is astronomical, and never part of a low-interest promotion. Cash advances are treated differently than regular purchases on credit cards.

When you take a cash advance, you are loaning yourself money – but the card company gets the interest.

In the past, credit card companies would always apply your payment to the lowest interest-rated balance on the card. This, of course, keeps you in debt longer, and allows the card company to make a bigger profit, since your interest payments are higher.

In 2010, a law came into effect in the United States that disallows this practice by credit card companies. Now, except for the minimum payment due, your payment will go toward the balance on your card that carries the highest interest rate, which works in your favor, unless you pay only the minimum balance. That amount, regardless, will go toward the lowest interest rated balance.

I’m still trying to find trustworthy information about a similar Canadian law, as well as laws in other countries, but so far, it looks like Canadian credit card companies, at least, are still applying payments to lower rated balances first. For this reason, I’m relieved to be able to say that I have never once taken a cash advance against a credit card – I think the only worse thing to do than this might be borrowing money against a future paycheck at a check-cashing outlet. I’ve never done that either, thankfully.

Always pay more than the minimum balance due on a credit card statement every, single month.

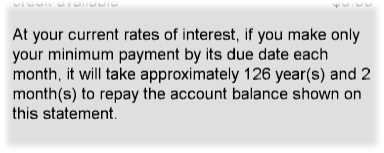

Here’s something that should scare the crap out of you…

This is a cut-and-paste from one of my credit card bills – sort of an “FYI” showing up at the bottom of the statement.

126 years.

Seriously. I don’t owe a whole helluva lot on this card, either. The only reason I’m not terrified by that screenshot is that I already have a date attached to Balance Zero on this card, and it’s only a few months away.

You can’t be afraid of your bills. Follow these rules, and you’ll get your credit card debt corralled and soon tamed.

That’s when the Money Game gets really interesting!

Stay tuned…

***

Want to play The Money Game with me, get out of debt and learn to live a Prepaid Life? Subscribe to the Debt Elimination category of posts in the form below.